In November 2016, European Payments Council (EPC) launched the SEPA Instant Credit Transfer scheme. With this move, the payment coordination body of the European banking industry has placed over 34 European countries at the center-stage of ‘mobile payments’. This scheme will not only spearhead adoption of instant mobile payments and transactions worldwide, but also push the major economies of the World to start regulating the unstructured and incomplete mobile payments legal framework. The 2012 statement by the Associate General Counsel of Board of Governors of the Federal Reserve System (BGFRS), United States, summarized the consumer regulations related to mobile payments that are still existent and followed in the US. Growing adoption of mobile payments and steps taken by other regulatory bodies of the world like EPC will certainly push USA to update its own regulatory and legal framework.

In November 2016, European Payments Council (EPC) launched the SEPA Instant Credit Transfer scheme. With this move, the payment coordination body of the European banking industry has placed over 34 European countries at the center-stage of ‘mobile payments’. This scheme will not only spearhead adoption of instant mobile payments and transactions worldwide, but also push the major economies of the World to start regulating the unstructured and incomplete mobile payments legal framework. The 2012 statement by the Associate General Counsel of Board of Governors of the Federal Reserve System (BGFRS), United States, summarized the consumer regulations related to mobile payments that are still existent and followed in the US. Growing adoption of mobile payments and steps taken by other regulatory bodies of the world like EPC will certainly push USA to update its own regulatory and legal framework.

According to a report by market intelligence firm International Data Corporation, the worldwide annual transactions volume of mobile payments is expected to cross US$ 1 trillion in 2020 from US$ 500 billion in 2015. It becomes an equally valuable question – who is filling this huge gap? The answer is spread across companies ranging from global tech giants like Google etc. to fintech companies like Paypal and other several startups. The adoption rate of products and services enabling mobile payments has been moderate and hence, it tends to raise questions on market traction and penetration in days to come. As stated earlier, the legal framework and operative guidelines from the regulatory authorities on mobile based payments have been absent until now – not anymore! Companies like Samsung, Apple and Google have patiently waited for this opportunity and have been slowly gathering mobile payments related patents. As the regulatory and legal framework takes shape and markets incline towards reliance on mobile payments, something long due will be set in motion too – patent licensing and infringement lawsuits.

Patent Landscape – Major Players

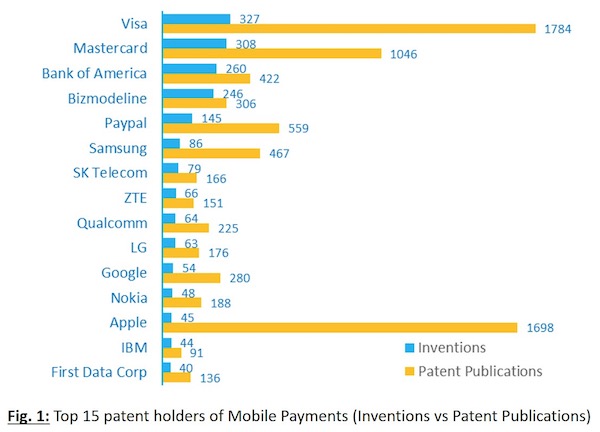

The patent landscape of mobile based payments should help in putting things into perspective. Fintech companies are ruling the patent realm. Visa and Mastercard dominate with over 300 worldwide patented inventions each. PayPal is expanding its digital presence by investing huge in acquiring promising startups. In 2015 alone, it bought four startups including Xoom Corp., a digital money transfer company for US$ 890 million and Paydiant, a mobile wallet company for US$ 280 million. With such acquisitions and strategic partnership with Mastercard since 2007, PayPal is clearly one of the strongest mobile payments contender.

Non-fintech companies are swiftly catching up too, owing to their strong smartphone market presence. Apple is placed at 13th position with respect to number of inventions but 2nd when it comes to the total number of patent publications (issued patents and pending publications). Samsung appears as the strongest competitor with 86 inventions and is placed ahead of all tech players. It acquired LoopPay, a mobile payments startup in 2015 for US$ 250 million and immediately rolled out tap-n-pay feature with its Galaxy S6. With this, Samsung is taking on potential market capturers like Apple Pay, Google Pay and PayPal-Mastercard partnership.

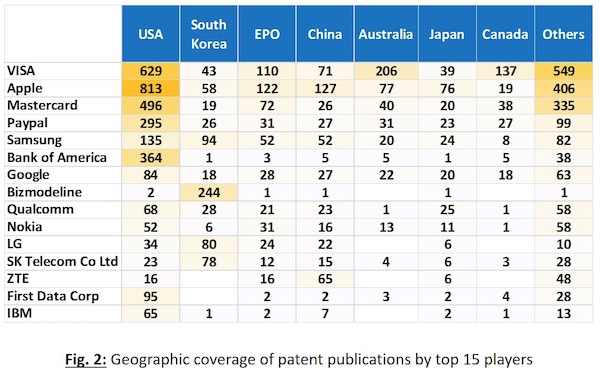

Figure 2 shows the geographic interests of the top 15 players with respect to the number of total patent publications. Besides USA, Korea is the key geography with impressive patent portfolios built by players like Bizmodeline, Samsung, LG and SK Telecom.

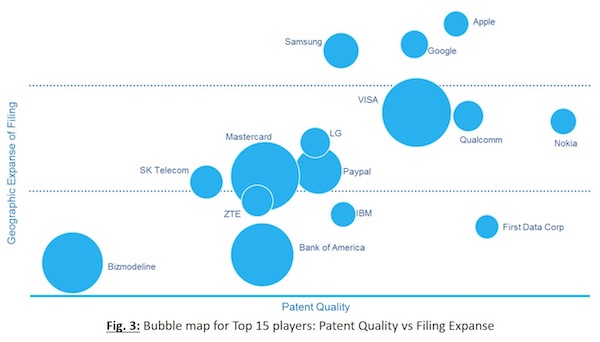

The bubble map (figure 3) shows comparative standings of these top 15 players with respect to their patent portfolios. The horizontal spread i.e. ‘patent quality’ has been prepared using our proprietary ‘patent quality scoring’ tool. The vertical spread i.e. ‘geographic expanse of filing’ refers to the stretch of jurisdictions in which inventions have been filed as patent applications. The size of a bubble corresponds to the number of inventions of that company related to mobile payments.

Concur IP’s ‘Patent Quality Scoring’ tool benchmarks individual inventions against each other in a patent collection based on the following parameters: forward citations, geographic filing stretch, issuance status, remaining life and IPC (International Patent Classification) codes based technical expanse.

Apple is a clear overall winner with a small yet powerful patent portfolio. Among the fintech companies, First Data Corp. has the portfolio with highest quality score followed by Visa and Paypal. This is mostly because First data’s portfolio is fairly younger and heavily cited by other parties. Bizmodeline is mostly concentrated in S. Korea with major focus only on contactless payments.

Since, fintech companies lack the in-house smartphone support, market speculations of their acquisition by any of the smartphone manufacturers like Apple and Samsung are imperative. Portfolios like Visa, Mastercard and Paypal are very lucrative for the surrounding companies. It isn’t too difficult to imagine how this bubble map would shape-up if any such acquisition happens.

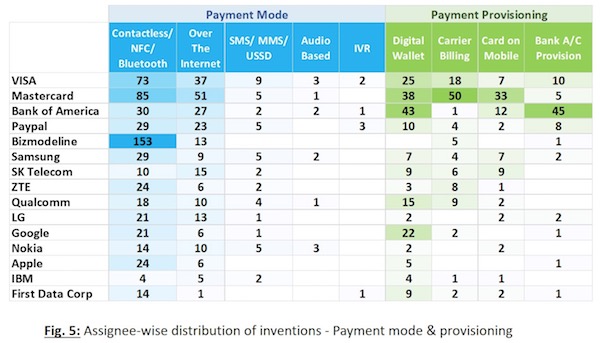

Payment Modes & Provisioning

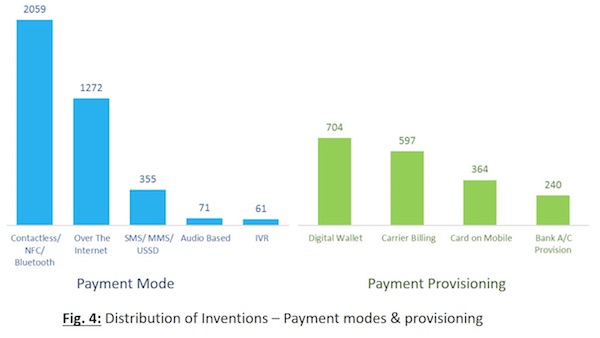

Let’s look at the enabling technologies and forms of mobile payments. Figure 4 shows the distribution of inventions among the payment modes and provisioning methods. Payment modes illustrate the underlying technologies used for mobile payments and provisioning refers to the payment tools.

While most common payment modes use contactless techniques (such as NFC) and over-the-internet, SMS/ MMS/ USSD based transactions can be quite fast and handy. Payment modes which use interactive voice response (IVR) over a phone call and audio based are less popular, relatively non-intuitive and insecure. Audio based mode includes Near-Sound Transfer, Data-over-Voice, audio signature and acoustic coupling. Digital wallet based payments are most prolific both in prevalent products and patented inventions. A payment provisioning method can be implemented using several modes. For example, a wallet based payment can be made using any one of several modes, NFC being the most popular.

Figure 5 illustrates the distribution of patented inventions for a) Payment Mode and b) Payment Provisioning among the top 15 assignees.

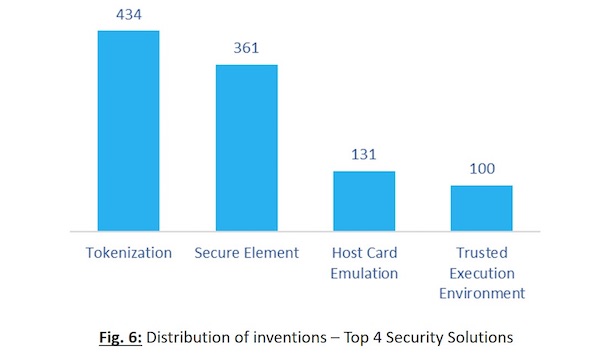

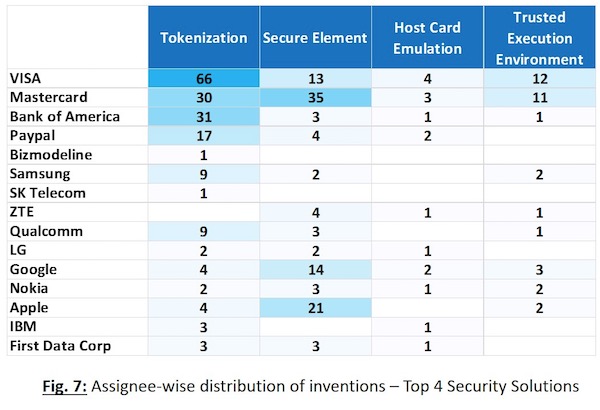

Security Solutions

As mobile payments become mainstream and widespread, transactional security is vital. The four security technologies at the center-point of mobile payments are Tokenization, Secure Element, Trusted Execution Environment and Host Card Emulation. While these solutions take care of the infrastructural security, extra layers of security at different levels are needed to complement these solutions. Biometric provisions like Touch ID in Apple Pay, security PIN, one-time-passcode, point-to-point encryption, 3D secure are some of the popular ones.

Let’s briefly discuss the top four technologies to better relate to the patenting trends of the top players among these candidates.

Let’s briefly discuss the top four technologies to better relate to the patenting trends of the top players among these candidates.

- Tokenization: Protecting sensitive financial information such as card number by replacing it with unique and virtual credentials called ‘tokens’. Visa leads with 355 patent publications (66 inventions) related to ‘tokenization’.

- Secure Element: A tamper-resistant chip or a SIM/ UICC card resident on the mobile phone that emulates a contactless card. Mastercard leads with 147 patent publications (35 inventions) related to ‘secure element’.

- Host Card Emulation (HCE): Unlike ‘secure element’, a payment card is emulated using either only software or cloud environment. Visa leads with 42 patent publications (4 inventions) related to HCE.

- Trusted Execution Environment (TEE): A secure portion of the mobile phone processor that offers end-to-end safe execution of ‘trusted’ applications by enforcing protection, confidentiality, integrity and data access rights. Visa leads with 42 patent publications (12 inventions) related to TEE.

Conclusion

According to a BCG report a whopping 3 billion users will rely on accessing internet-based services on mobile by 2020. This is a huge market and mobile based payments is undoubtedly the future of digital money transfer, commerce and banking. Looking at the distribution of technology and patents, the power lies mostly divided between fintech and non-fintech companies. Hence, mergers and acquisitions will become more prominent in times to come and so will patent infringement lawsuits. When chip giant Qualcomm announced to acquire NFC pioneer NXP Semiconductors for US$ 47 billion earlier in 2016, it clearly indicated that Qualcomm has strong intentions to catapult its way into mobile payments, apart from Internet-of-Things and connected devices.

Mobile based payment is complex business area and is still evolving. To offer comprehensive services in compliance with the upcoming regulatory guidelines and security benchmarks, it will become almost impossible for a company X offering a service, for example mobile wallet, to bypass using a security solution like ‘tokenization’ patented by company Y. A 2016 Bloomberg report highlights the seriousness with which fintech companies are taking their patent portfolio and how they intend to compete with the tech giants in asserting their IP. Since, mobile phone manufacturers are the front-end contenders, it gives them even stronger reason to assess the technology, competitive standings and patent landscape of mobile payments. Building a streamlined patent portfolio by identifying technology trends and filling the corresponding gaps can prove crucial. It will not only enable the phone makers to offer more robust mobile payment services but also prepare for the upcoming patent wars.

Disclaimer – The opinions expressed in this article are author’s personal opinions and do not constitute a legal advice. The author or his firm Concur IP Consulting is not involved in practice of law.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/UnitedLex-May-2-2024-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

4 comments so far.

Vivek Sharma

January 13, 2017 03:04 amAs discussed with you over email, the article is based on the count of INPADOC patent families (inventions). The number of INPADOC families should not be interpreted as a reflection of total number of patent publications.

Michelle Fisher

January 6, 2017 04:18 pmVivex

I read your report on mobile payment IP.

There are a few companies you missed including ours. See the reports below:

https://www.linkedin.com/pulse/nfc-patents-smartphone-mobile-payment-data-2q-2016-alex-g-

http://techipm-innovationfrontline.blogspot.com/2015/03/nfc-patents-for-standards-applications.html?m=1

Michelle Fisher

January 6, 2017 12:20 pmhttp://techipm-innovationfrontline.blogspot.com/2015/03/nfc-patents-for-standards-applications.html

Michelle Fisher

January 6, 2017 12:20 pmHi Vivek, here are some other reports that might be useful

https://www.linkedin.com/pulse/nfc-patents-smartphone-mobile-payment-data-2q-2016-alex-g-

html