Intellectual Property (IP) is a crucial portion of a company’s assets. Today, a great portion of the assets of fortune 500 companies consists of intangible assets including intellectual property.

Intellectual Property (IP) is a crucial portion of a company’s assets. Today, a great portion of the assets of fortune 500 companies consists of intangible assets including intellectual property.

A strong IP portfolio is instrumental for fundraising, leverage in business transactions, exit strategy (e.g. for startups), and business transactions such as mergers and acquisitions (M&A), to name a few.

Intellectual property may consist of patents, trademarks, copyright, and trades secrets. Patents are in many cases the most important portion, especially in the high tech and biotech industries. Since there are a large number of transactions in these areas, it is important to assess and estimate the value of a patent portfolio.

A strong patent portfolio provides confidence and relative freedom to operate (FTO) for mid-range and large companies. For smaller companies and startups eyeing an exit scenario, an FTO analysis based on their patent portfolio is usually a big factor in the total company valuation. It is for this reason that patent portfolio valuation has become a major discipline in high demand.

Even though patent sale transactions have been around for more than a century, in recent years, such transactions have become a market in their own right. Significant transactions have taken place worth up to billions of dollars per portfolio with direct or indirect bidding (through a proxy). Examples include the sale of the Nortel, Motorola Mobility, and some of Eastman Kodak portfolios.

Philosophy of an IP Market

Patents have grown from more fancy and honorary pendants to all-out financial assets and they have created their own market. This is partly due to increasing abstraction of business moving from more tangible businesses and assets to more intangible ones. Abstraction of business started a long time ago. The more abstract a line of business, the more sophisticated the methods used to conduct that line of business, and the more profitable and scalable. However, this abstraction of value comes with some risk.

In the past few decades, the pace and speed of technological advances has resulted in an increasing trend of products and services being rapidly commoditized by new products and services, which create new markets. We have witnessed chips being commoditized by systems and, systems by software, by advertisements and services that scale business opportunities at never before experienced levels. These products and services are becoming more and more abstract and intangible.

This trend inevitably carries through to patentable ideas as the ultimate abstraction of business products and services. This gives rise to an emerging IP market as witnessed in the last two decades.

A result of this is vertical integration, of which all tech giants are excellent examples, each having its own devices, software, cloud services, and e-commerce. All these tech heavyweights are filing an increasingly massive number of patents too. Before one is commoditized by someone else, one invents oneself into the next business level.

Examples of Early Patent Transactions

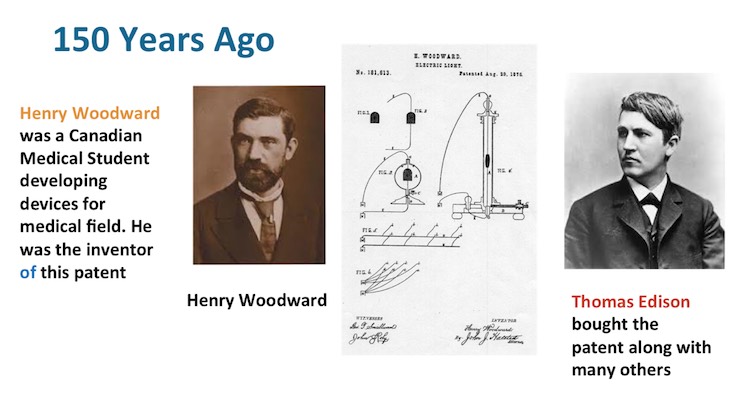

Despite the recent emergence of IP market, it is not a new phenomenon. Such transactions have taken place for more than a century. Here is an example from about 150 years ago shown in figure 1 when, in pursuit of rights to the electric light bulb, Thomas Edison bought a patent from a Canadian medical student by the name of Henry Woodward.

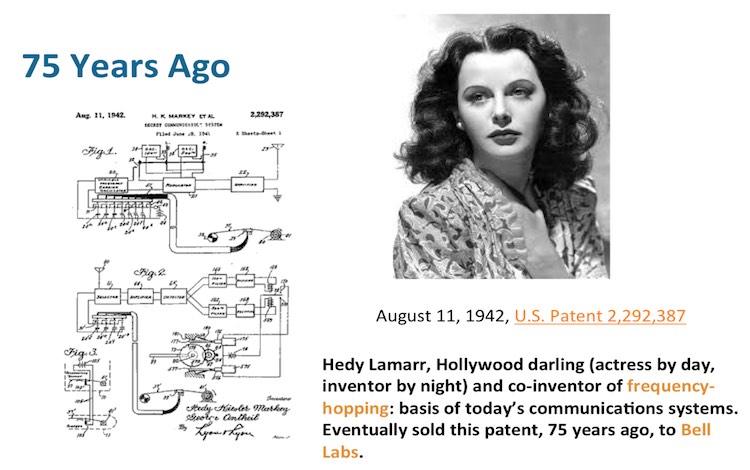

Here is another historically significant transaction around 75 ago shown in figure 2: Hedy Lamarr, Hollywood darling, actress by day and inventor by night, was the co-inventor of a frequency-hopping patent, which she eventually sold to Bell Labs. This technology turned out to be the basis of today’s communications systems.

Portfolio Valuation Methods

Now that we know patents are assets, the question would be how much is a patent worth? And how can one estimate a patent’s value?

Basically, there are three fundamental methods for patent valuation

- The first one is cost-based valuation which attempts to estimate the cost of generating a patent including R&D, legal, fees etc. This method, as we will see, indicates that a patent should be worth at least $50K.

- The second method is market-based valuation, which is basically a like-for-like comparison. Spanning from covering peripheral features to a core technology features, a patent could be worth from $50k to more than $250k.

- The third method is income-based, which, in essence, is the amount of money:

- one could make with the patent through monetization

- would otherwise cost one to obtain rights to the patent.

We will now explain these three methods in more detail.

Cost-Based Valuation

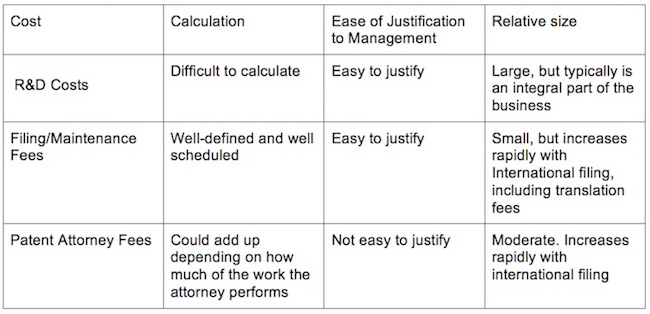

Cost-based patent portfolio valuation estimates the incurred cost to generate an innovative idea, file for a patent, and maintain the patent. These costs are summarized in the following table.

As seen from the table, these costs are varied dramatically and some of them are hidden and considered necessary for the business of the company anyway.

Developing patents really depends on how IP-savvy a company is. There are two mainstream schools of thought. One believes in filing patents only if absolutely necessary. This school is quite lethargic and reluctant in developing IP portfolios. The other school is always on top of the task of developing a patent portfolio and they go out of their way to put the right people on the task.

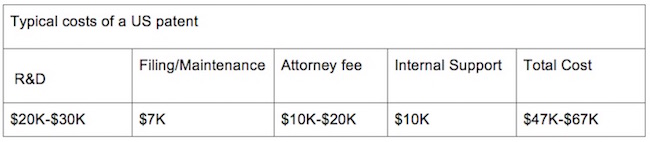

Here we bring typical costs of developing a US patent in US dollars.

As seen from the table, on the average, a quick estimate of the cost of a patent yields $50K+ per patent. For a patent filed internationally, including foreign filing fees, translation fees, and foreign associate fees, the total figure easily reaches $100k+. This tells us that, if a patent is of interest, it cannot be worth less than $50K.

In reality, however, we know the value of a patent, regardless of costs, could be anywhere from zero to millions of dollars. As the IP market gets more and more mature, we expect the cost-based method to be less and less used. There are, however, quite a few M&A (Mergers and Acquisition) and investment outfits who are still using this method along with market-based patent valuation described below.

Market-Based Valuation

The market-based method attempts to use a like-for-like analysis of patent prices. In doing so, for a given patent portfolio, this method looks for comparables. Market-based valuation of portfolios require that the portfolios considered are comparable in technology, size, and quality.

Traditionally, the market-based method works well for tangible assets. A prominent example of this is real estate. In this industry, two houses in the same neighborhood, with same age, condition, and size, present good comparables.

For intangible assets, and especially with patents, this method might not be quite accurate depending on the size of the portfolio. For one thing, unlike real estate, of two very similar patents, one might be invalid just by the virtue of being filed after the other one.

For larger portfolios, however, this problem goes away. The risks of invalidity and lack of infringement decrease rapidly with the number of patents in a portfolio.

A good example of comparables that is often referred to is the Nortel LTE Portfolio sold for $4.5B to Rock Star Alliance (formed by Apple and Microsoft and a few other partners). An alliance including Google and Intel was bidding in that auction too. Later on Google acquired a similar portfolio of LTE essential patents from Motorola Mobility for a comparable price of $5.5B. This was after Google acquired the company for $12.5B and got some cash and spun off the rest of the company for about $7B. Other example of large portfolio transactions in recent times includes portfolios from Eastman Kodak (for which the author of this article managed the valuation team), AOL, and AMD.

Even though the market-based valuation method breaks down for small portfolios, and especially for a single patent, there are certain measures one could use to mitigate this shortcoming. For instance, if one needs to use market-based valuation for a single patent, here are the steps one could take

- Ensure the validity of the subject patent

- Identify a claim read on a product feature

- Identify how core that feature is to the product

- Find a similar patent involved in a recent transaction

- If core features are different, use modeling to correct

- Estimate the market-based valuation

- Finally, assess risks and use as discount factor

Income-Based Valuation

Income-based based valuation is an estimation of how much income a patent portfolio could generate over a specific period. Another way to consider this for a defensive practicing entity is to consider what business size it protects and what is the business cost of not owning or not having rights to a patent portfolio.

The income-based method is the most reliable and most utilized method in the patent market, and as such, it has been utilized increasingly more often in recent years and replaced the other two methods.

The income an entity could generate is usually calculated by a discounted cash flow model from monetization schemes such as those indicated in table below.

Any combination of the above could also be used and, as one could guess, it complicates the discounted cash flow model by the same token.

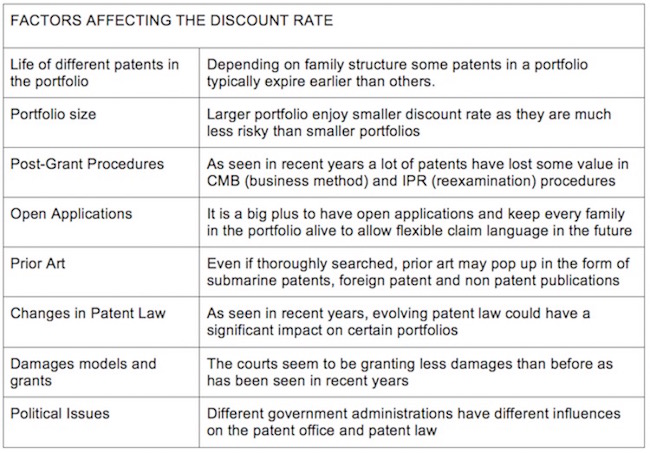

In a discounted cash flow model, there are many factors that affect potential royalty rates and the various discount factors and rates. Here is a summary of such factors:

With the example numbers given in the table above, multiplying all the factors one gets:

Final Factor : 0.05 x 0.1 x 0.01 x .01 = 0.000005 or 5 parts in a million of revenue.

In this case, for a smartphone worth $700, the royalty per unit would be:

0.000005 x 700 = 0.0035 or 0.35 cents per unit.

This number, even though seemingly low (third of a penny), is non-trivial and it is often highly contested. A company may sell some 200 million mobile devices per year. This would amount to an annual royalty rate of:

0.0035 x 200,000,000 = $700,000 or 700 thousand dollars.

Bear in mind that this is for a single patent and only one company for licensing was considered. For a portfolio on smartphones including many patents on each technology or sub-technology of the mobile device, this could really add up to tens, possibly hundreds of millions of dollars. Add to that the fact that there are many sizable portfolios of this nature. This is why licensing negotiations or proposals are so highly contested.

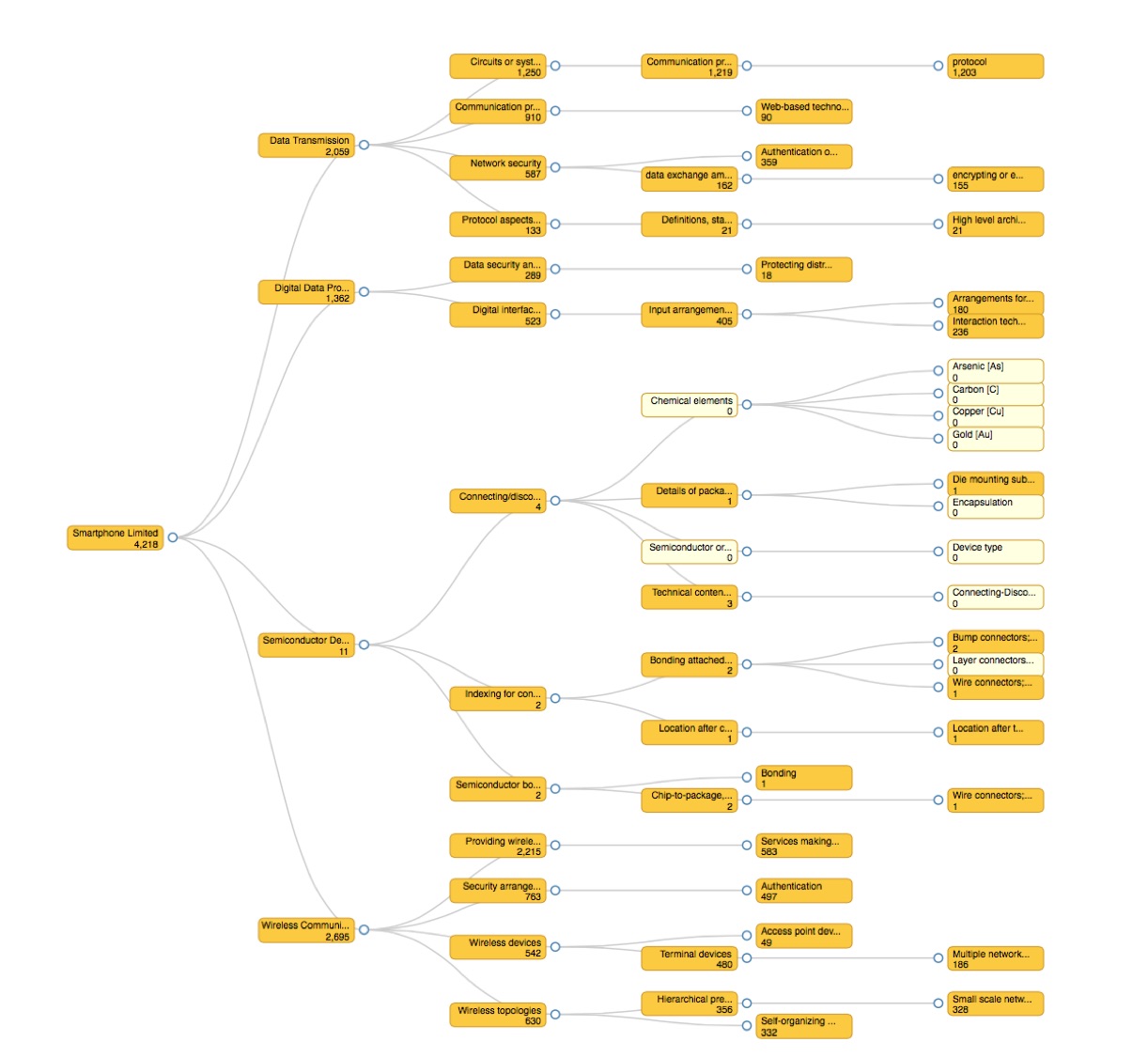

To shed some light on the enormity of licensing or monetization opportunities in this area, here in figure 3, we bring a taxonomy generated by the Relecura patent search tool of about 4000 selected families of patents related to smartphones:

One could see that, for these selected 4000 patents, there are many nodes of the taxonomy that are nicely populated, indicating many features of a smartphone on which a patent portfolio may read.

When calculating royalties for the coming years, there are various inputs that give rise to a discount rate that chips away from future annual royalties in a compounding manner.

Putting all these risks into perspective, the discount rate normally lands between 10% to 25%. This factor is another highly contested issue in licensing negotiations as it has a huge impact on the future revenue from licensing.

Additional Factors in Valuation

It is important to determine all the encumbrances of a portfolio. Sometimes a prospective seller claims that they have only licensed 40% of the market and the remaining 60% is unencumbered. Even though this statement might be completely true, a close look at the unlicensed segment might reveal that the remaining 60% of the market is highly fragmented and there are too many players, whereas the licensed 40% represents only two or three big companies. It is well known that a disparate market is very difficult to license, and that is often exactly the motivation behind selling off such portfolios.

Another big dispute item is indemnifications. A potential argument against a licensing proposal, say for a patent that reads on a smartphone battery, is to say that the smartphone maker is indemnified by the battery vendor. However, the counter-argument would be to ask if the battery component is bought off the shelf or if it is custom-made. The answer to this question is, without an exception, the latter. As such, it will be difficult argument to use indemnification for refusing to obtain a license to the portfolio.

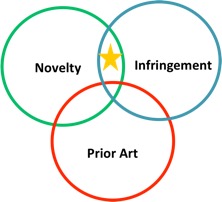

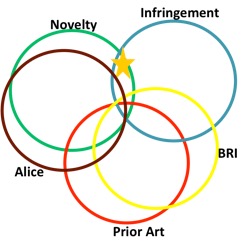

One way to think of the outstanding factors when valuating a patent portfolio is to think of this diagram and try to steer clear of risk areas. The region indicated by the star in figure 4 is the sweet spot for a valuable patent.

In recent times it might be even more beneficial to think of additional but close circles which would include steering away from Alice (statutory subject matter) and broadest claim reinterpretation (BRI) issues. Generally, there is a greater value when a patent is closest to the region indicated by the star in figure 5. The farther one moves away from the star, the more risk and discount would apply.

Future Value Estimation

A big question that may arise is valuating a potential future value. A patent portfolio may have assets or might be entirely consisting of patents covering technologies that are not in use today but are future bets. It is very difficult to identify future value and to estimate the value of such portfolios, however, there are certain measures and factors one could exploit.

The main premise is great future rewards vs. potential risks of failure. The risk factor might be taken as a discount factor and factored in to the potential royalty calculations.

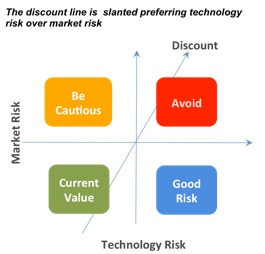

Generally there are two major types of risk when considering future value in patents:

- Market Risk – This is the risk that the technology may never have a substantial market. Perhaps one example is chatbot initiatives which are going on in the US to mimic WeChat of China. However, that market may be a match for the Chinese culture and business but may not culturally or commercially become as popular in the West. Market risk is a tougher risk to take.

- Technology Risk – Here there is little or no doubt that there will be a market for the claimed technology/invention, but the risk is that it may fail or lose to a competitive technology.

An example of technology risk in potential patent valuation is portfolios related to resistive memory or phase change memory which are currently not used on a commercial scale. However, memory will be needed in the future. This is a good risk to take.

Figure 6 is a diagram that shows Technology Risk vs. Market Risk and a recommendation of placing the discount factor. As could be seen, technology risk is often preferred over market risk. That is the reason the discount line is not at 45 degrees but rather tilted towards the market risk axis.

A word of caution about assessing market risk: Certain areas, like RNA Epigenetics, for which there is no really good solution right now, don’t have a great market. However, this doesn’t mean there will be no great market in the future. A good technology will change this and the market will be there in great demand.

Valuation of Standard Essential Patents and the FRAND Issue

Standard Essential Patents are traditionally very valuable but recently have been compromised by fair-reasonable and non-discriminatory (FRAND) measures in different jurisdiction.

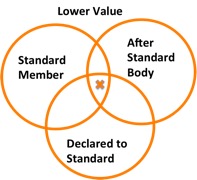

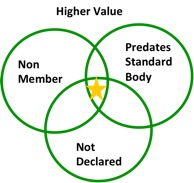

There are certain factors and circumstance that would still render a standard essential patent very valuable. Here is a hierarchy of value in Standard Essential Patents, in ascending order of value:

- Belongs to Standard Committee member and is declared

- Belongs to Standard Committee member but not declared

- Belongs to Standard Committee member with priority date before the committee was sitting

- Belongs to a non-member

- Belongs to a non-member with priority date before the Standard Committee was sitting

As such, here is the lower-value circles shown in figure 7, and the higher-value circles shown in figure 8 with respect to FRAND.

A valuable standard essential patent would then be close to the star in figure 8 and away from the cross in figure 7.

Besides direct SEPs there is the category of patents described as “Standard plus Feature” or “Standard+”. These patents, by virtue of adding a proprietary feature which enables certain functionality to an otherwise standardized technology, may escape FRAND obligations. An example of such a patent would be a portable medical device using communications standards.

Valuation Cross-Calibration

Different valuation methods could be used for benchmarking and cross calibration of each other and for portfolios of future value.

Market-base data of transactions, which have already closed, could be used for benchmarking income-based methods in a way to re-calibrate different coefficients and different discount factors and rates and, in particular, royalty stack considerations.

Another useful calibration is using current value estimation of certain portfolios as a benchmark for future value of other portfolios. For example, a portfolio in memory technology could be used to estimate the value of a portfolio in resistive memory which may be a future bet.

Moreover, different portfolios covering different technologies of the same product could be used to benchmark each other so long as both technologies are core to the product and the portfolios are roughly the same size and stature.

In addition, so far as future value is considered, portfolios covering different competing technologies could be used to benchmark against each other. For example portfolios covering resistive memory and phase-change could be used for benchmarking each other.

For emerging technologies, a portfolio from one emerging technology could be used to benchmark one in a completely different field. For example Fintech portfolios and Autonomous Vehicles portfolios could be roughly benchmarked against each other.

Thee checks and balances could be placed to ensure consistent and reasonable valuation results.

Conclusions

IP valuation, and in particular patent portfolio valuation, is playing an ever increasing role in today’s business transactions. With patents becoming a great portion of the assets of any company, many professionals need to deal with patent portfolio valuation for a variety of purposes.

Even though traditionally valuation professionals have used a combination of cost-based and market-based valuation, more and more practitioners are using income-based valuation in combination with market data. The income-based model focuses on what potential monetization or potential impact on business a patent portfolio might have, and as such, it is much more dynamic and reliable.

For patent portfolios of potential future value, technology risk is preferred over market risk and one could use current market data to benchmark future value while building an income-based valuation model.

As to standard essential patents and FRAND obligations, highest value patents are the ones not declared to the standard and belonging to standard committee non-members, with a priority date before the committee is established. Another valued category is “standard plus function” patents.

The increasing patent filing of large companies, and the healthy activity in small and mid-size companies is a good indication that the patent market will remain healthy and patent portfolio valuation will play a crucial role in many business transactions. While the market may go through transformations, it is going to be there for decades to come and there will be an increasing need for professionals specializing in patent portfolio valuation.

Please Note: This article has been updated on July 17th to include the images and figures that were originally missing from the post. This was an error on my part, as we were handling a family emergency. My apologies to the author, Dr. Masoud Vakili and you the reader as well.

Renee C. Quinn

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/UnitedLex-May-2-2024-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

One comment so far.

Renee C. Quinn

July 17, 2017 03:02 pmPlease Note: This article has been updated on July 17th to include the images and figures that were originally missing from the post. This was an error on my part, as we were handling a family emergency. My apologies to the author, Dr. Masoud Vakili and you the reader as well.