Bank of America, by Mike Mozart

The Bank of America is a multinational corporation based in Charlotte, NC, that provides banking and other financial services to customers all over the world. As of 2010, this company placed 3rd on the Forbes Global 2000 list of the world’s biggest companies by sales, profits, assets and market value.

In order to stay atop the world of financial services, the Bank of America is forced to be very innovative especially given the rise of mobile banking services and financial cybersecurity risks. Recently, Samsung announced BofA as a launch partner of its Samsung Pay mobile pay service along with JPMorgan Chase, Citigroup and US Bancorp; all four of these banks are also members of Apple Pay as well. Much of BofA’s ability to innovate comes from strategic startup acquisitions and its most recent Technology Innovation Summit identified 30 startups out of the 200 which presented technologies to the banking giant that the company will add to its roster of vendors. This focus on identifying useful innovation from outside of the company is a trend in the banking industry that extends far beyond the Bank of America.

The most recent earnings report issued by Bank of America for the fourth quarter of the 2014 fiscal year indicated that the company reported a quarterly net income of $3.1 billion, a reduction compared to the $3.4 billion net income enjoyed by the company in the previous year’s fourth quarter. It’s not clear if lower revenues are a cause, but shareholders have been asking the company for a greater degree of power in corporate decisions and BofA has been acquiescing. In mid-March, the company announced that shareholders  owning at least three percent of company stock for three years would be granted proxy access for nominating potential board of directors members. Thanks to a recent U.S. Securities and Exchange Commission decision, shareholders attending the Bank of America’s annual shareholder meeting will also be able to vote on whether the corporation should divest itself of its holdings in Merrill Lynch.

owning at least three percent of company stock for three years would be granted proxy access for nominating potential board of directors members. Thanks to a recent U.S. Securities and Exchange Commission decision, shareholders attending the Bank of America’s annual shareholder meeting will also be able to vote on whether the corporation should divest itself of its holdings in Merrill Lynch.

During 2013, the Bank of America came in 130th overall among companies earning patents from the U.S. Patent and Trademark Office with 262 U.S. patents granted in that year. This total was nearly 60 percent greater than the number of U.S. patents earned by the firm during the previous year. Patent portfolio analysis tools powered by Innography are showing us that BofA was assigned 251 U.S. patents during 2014. Unsurprisingly, most of these innovations are focused on financial institutions, financial transactions and user accounts. However, as the text cluster will show our readers, we did notice some intriguing areas of development in mobile devices, especially regarding real-time video and authentication requests.

[Companies-1]

Bank of America’s Issued Patents: From Mobile Device Transactions to ATM Video Services

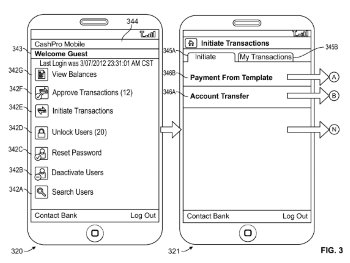

Mobile devices were the subject of a pair of recently issued Bank of America patents recently. It was at least a little intriguing, however, that the invention relates more to personal security than the protection of financial accounts. U.S. Patent No. 8922657, entitled Real-Time Video Image Analysis for Providing Security, claims a method for providing security to a user by receiving an image of an area frequented by a user, building a directory of non-human object and individual data within that area, recognizing variations between the data directory and a real-time video stream of the area and presenting selectable indicators of recommended security actions associated with the variations to a user via a mobile device. The innovation is intended to provide smartphone owners and other mobile device users with an augmented reality service for identifying unwanted home intrusions and offer them options for contacting authorities. Bank of America has also made more headway into the  rapidly growing mobile banking field thanks to the recent issue of U.S. Patent No. 8914308, which is titled Method and Apparatus for Initiating a Transaction on a Mobile Device. This patent claims a method for displaying the initiation of a transaction on a device by using a processor to display an initiate transactions template display window, find and select a template from a list of templates, display a detailed template display window showing at least one detail of the selected template, convert the detailed template into a reviewable transaction in response to a user input, display a review/submit display window showing a list of reviewable transactions and initiating a reviewable transaction in response to a user input. This invention represents an enhanced treasury management system which is optimized for small electronic devices like smartphones, which have limited screen sizes.

rapidly growing mobile banking field thanks to the recent issue of U.S. Patent No. 8914308, which is titled Method and Apparatus for Initiating a Transaction on a Mobile Device. This patent claims a method for displaying the initiation of a transaction on a device by using a processor to display an initiate transactions template display window, find and select a template from a list of templates, display a detailed template display window showing at least one detail of the selected template, convert the detailed template into a reviewable transaction in response to a user input, display a review/submit display window showing a list of reviewable transactions and initiating a reviewable transaction in response to a user input. This invention represents an enhanced treasury management system which is optimized for small electronic devices like smartphones, which have limited screen sizes.

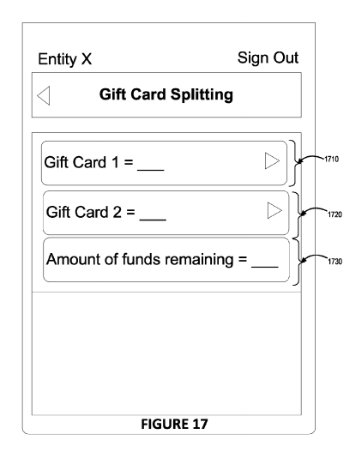

A couple of Bank of America patents protect interesting business tools that may benefit a variety of merchants. A more robust system for providing gift cards to consumers which can be used with a variety of merchant partners is the focus of U.S. Patent No. 8973819, issued under the title Gift Card Splitting. It discloses an apparatus for splitting a gift card which includes a processor for executing instructions that receives information associated with a gift card, associates the gift card with a first user account, determines that the user is within a distance of the merchant based on GPS coordinates, transmitting a message to the first user’s mobile device including a new offer for a second merchant with an expiry date based on the gift card’s age and a period of inactivity and enables the option of splitting the gift card into multiple portions. The system supported by this invention allows a consumer to utilize funds associated with multiple gift cards using a single payment method through an associated user account. Enhanced billing data systems that achieves a reduction in the amount of billing rejects from customers are outlined within U.S. Patent No. 8977564, which is titled Billing Account Reject Solution. It protects computer-executable instructions which perform a method for validating an account number by using a first receiver to receive an employee identification number input into a graphical user interface (GUI), receiving a billing account number input into a GUI, determining if the billing account number includes a threshold number of consecutive, identical digits, transmitting a data file including the employee ID number and the billing account information to a predetermined e-mail address if the threshold is passed or accessing a database including valid billing account numbers and electronically identifying an account number included in the database that is identical to the billing account number. This system automates the process of identifying the root cause of billing rejects, which can be caused by outdated customer account information, and quickly notifying management staff of the situation.

A couple of Bank of America patents protect interesting business tools that may benefit a variety of merchants. A more robust system for providing gift cards to consumers which can be used with a variety of merchant partners is the focus of U.S. Patent No. 8973819, issued under the title Gift Card Splitting. It discloses an apparatus for splitting a gift card which includes a processor for executing instructions that receives information associated with a gift card, associates the gift card with a first user account, determines that the user is within a distance of the merchant based on GPS coordinates, transmitting a message to the first user’s mobile device including a new offer for a second merchant with an expiry date based on the gift card’s age and a period of inactivity and enables the option of splitting the gift card into multiple portions. The system supported by this invention allows a consumer to utilize funds associated with multiple gift cards using a single payment method through an associated user account. Enhanced billing data systems that achieves a reduction in the amount of billing rejects from customers are outlined within U.S. Patent No. 8977564, which is titled Billing Account Reject Solution. It protects computer-executable instructions which perform a method for validating an account number by using a first receiver to receive an employee identification number input into a graphical user interface (GUI), receiving a billing account number input into a GUI, determining if the billing account number includes a threshold number of consecutive, identical digits, transmitting a data file including the employee ID number and the billing account information to a predetermined e-mail address if the threshold is passed or accessing a database including valid billing account numbers and electronically identifying an account number included in the database that is identical to the billing account number. This system automates the process of identifying the root cause of billing rejects, which can be caused by outdated customer account information, and quickly notifying management staff of the situation.

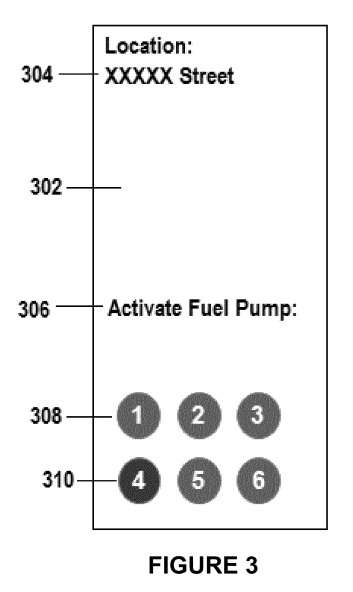

A system designed to help a consumer make better purchasing decisions when buying gas for their vehicle is discussed within U.S. Patent No. 8965790, which is titled Readable Indicia for Fuel Purchase. The mobile apparatus for purchasing fuel for a vehicle from a fuel station protected here involves a computing module configured to initiate a fuel purchase application on the apparatus, determine identification information associated with a fuel pump that will be used to fuel a vehicle and transmitting a purchase authorization request to an external server which determines a payment amount or a discount eligibility; the external server also processes the purchase authorization request, transmits an electronic receipt to the apparatus and authorizes the activation of the fuel pump. This invention is capable of helping a user understand how much money it will cost to fill their vehicle’s fuel tank to a predetermined capacity.

A system designed to help a consumer make better purchasing decisions when buying gas for their vehicle is discussed within U.S. Patent No. 8965790, which is titled Readable Indicia for Fuel Purchase. The mobile apparatus for purchasing fuel for a vehicle from a fuel station protected here involves a computing module configured to initiate a fuel purchase application on the apparatus, determine identification information associated with a fuel pump that will be used to fuel a vehicle and transmitting a purchase authorization request to an external server which determines a payment amount or a discount eligibility; the external server also processes the purchase authorization request, transmits an electronic receipt to the apparatus and authorizes the activation of the fuel pump. This invention is capable of helping a user understand how much money it will cost to fill their vehicle’s fuel tank to a predetermined capacity.

The Bank of America has been experimenting with the use of live video feeds to connect consumers to bank tellers at ATMs and we found an intriguing addition to this company’s IP portfolio in this sector in U.S. Patent No. 8941709, entitled Video-Assisted Self-Service Transaction Device. This patent protects a method of detecting an error associated with a transaction being made by a user at a self-service video transaction device, identifying a video agent terminal with video and audio functionalities to service the transaction error, determining whether a connection wait time for the video agent terminal exceeds a threshold time and sending instructions to print an error receipt containing contact information and a transaction error identifier for a user to rectify the problem. The system is designed to either provide a mechanism for contacting an agent through a video service to fix a transaction issue or issue a receipt with more information if no video agents are available.

Patent Applications of Note: From Better Goal Management to More Mobile Payments

We did finally notice a Bank of America innovation related to the world of cybersecurity once we surveyed the corporation’s patent applications recently filed with the USPTO. U.S. Patent Application No. 20150067862, filed under the title Malware Analysis Methods and Systems, would protect a system of installing a malware sample onto a virtual machine, analyzing the behavior of the malware sample, booting a physical computing device from a secondary boot source, installing the malware sample onto the physical computing device, again analyzing the malware sample’s behavior, determining whether the analyzed behaviors were different in any way and generating a notification of any analyzed differences. This innovation is designed to improve the detection of viruses, Trojan horses and other cyber attacks even when those attacks are very complex.

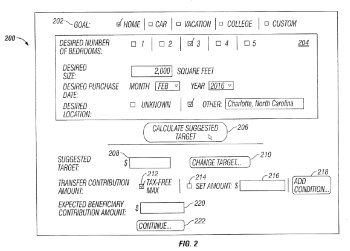

A couple of patent applications filed by BofA profile some interesting advances in various mechanisms developed to improve the savings abilities of its customers. A system that helps customers more effectively save money for college tuition, a car or other major expenditures is at the center of U.S. Patent Application No. 20150066722, which is titled Management of Contributions for a Goal. It claims a server for managing a contribution for a goal which includes a memory with a rule associated with a maximum contribution amount towards a monetary target and a processor that determines the monetary target associated with a goal shared between a contributor and an heir-beneficiary, determines a current saving level toward the target, determines whether certain agreed-upon savings conditions have been satisfied, calculates an amount for a contribution for a period of time and facilitating the transfer of the calculated amount. This system supports a savings mechanism towards a goal that improves upon personal goal saving methods which can typically be haphazard. The optimization of savings accounts for small business associations in the face of federal regulations is discussed within U.S. Patent Application No. 20150073993, entitled Savings Sweep Program. The system for linking customer checking and savings accounts within a financial institution to distribute funds between accounts claimed here includes a processing device executing code to receive input values for an upper limit, a lower limit and a target balance for a checking account, transfer a portion of checking account funds above the upper limit to an interest bearing savings account and sweeping a portion of a savings account into the checking account when the checking account balance falls below the lower limit. This system is intended to maximize the interest earned on business cash deposits made by a small business association while maintaining liquidity; it also complies with federal regulations that place a limit on the number of transfers between financial accounts without being physically present at the bank branch where the transfer order is made.

A couple of patent applications filed by BofA profile some interesting advances in various mechanisms developed to improve the savings abilities of its customers. A system that helps customers more effectively save money for college tuition, a car or other major expenditures is at the center of U.S. Patent Application No. 20150066722, which is titled Management of Contributions for a Goal. It claims a server for managing a contribution for a goal which includes a memory with a rule associated with a maximum contribution amount towards a monetary target and a processor that determines the monetary target associated with a goal shared between a contributor and an heir-beneficiary, determines a current saving level toward the target, determines whether certain agreed-upon savings conditions have been satisfied, calculates an amount for a contribution for a period of time and facilitating the transfer of the calculated amount. This system supports a savings mechanism towards a goal that improves upon personal goal saving methods which can typically be haphazard. The optimization of savings accounts for small business associations in the face of federal regulations is discussed within U.S. Patent Application No. 20150073993, entitled Savings Sweep Program. The system for linking customer checking and savings accounts within a financial institution to distribute funds between accounts claimed here includes a processing device executing code to receive input values for an upper limit, a lower limit and a target balance for a checking account, transfer a portion of checking account funds above the upper limit to an interest bearing savings account and sweeping a portion of a savings account into the checking account when the checking account balance falls below the lower limit. This system is intended to maximize the interest earned on business cash deposits made by a small business association while maintaining liquidity; it also complies with federal regulations that place a limit on the number of transfers between financial accounts without being physically present at the bank branch where the transfer order is made.

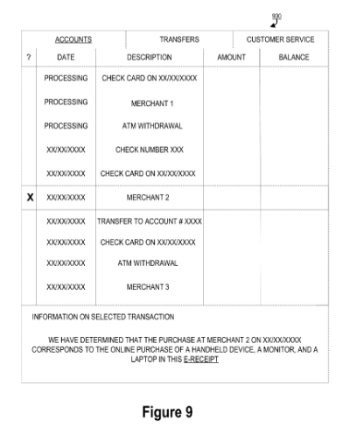

Novel lending mechanisms that provide a peer-to-peer platform to serve as an alternative for obtaining a loan to those with low credit ratings is described by U.S. Patent Application No. 20150058197, filed under the title Networking Platform for Lending. It claims a lending network system that includes a processing device that receives a loan request referral from a traditional financial institution or potential borrower information from an institution that had previously declined to fund the borrower, presents one or more potential lenders which aren’t associated with the institution to a potential borrower, receives an intent to fund at least a portion of the potential borrower’s loan request and facilitating a loan agreement between the borrower and lender. Other digital tools which would help financial account owners more effectively determine their budget for certain personal expenditures are featured within U.S. Patent  Application No. 20150032581, entitled Use of E-Receipts to Determine Total Cost of Ownership. This patent application would protect a system that includes a processing device executing program code to identify electronic communications between a customer and a merchant, extract purchase transaction data from the electronic communications, convert purchase information data into a structured format compatible with an online banking application, integrating the data into the application so a customer can access that information and determining an estimated total cost of ownership of a product based on the product’s purchase price and other costs associated with that product. This invention is configured to integrate online and offline purchase data so that an individual can view all costs associated with a certain product, such as a total cost for a vehicle that includes fuel and insurance costs.

Application No. 20150032581, entitled Use of E-Receipts to Determine Total Cost of Ownership. This patent application would protect a system that includes a processing device executing program code to identify electronic communications between a customer and a merchant, extract purchase transaction data from the electronic communications, convert purchase information data into a structured format compatible with an online banking application, integrating the data into the application so a customer can access that information and determining an estimated total cost of ownership of a product based on the product’s purchase price and other costs associated with that product. This invention is configured to integrate online and offline purchase data so that an individual can view all costs associated with a certain product, such as a total cost for a vehicle that includes fuel and insurance costs.

The Bank of America is concerned with building more effective financial tools for business clients as well as individual consumers as is reflected by U.S. Patent Application No. 20150073873, titled Automated, Self-Learning Tool for Identifying Impacted Business Parameters for a Business Change-Event. It would protect an apparatus with a business parameter impact determining tool stored in a memory which is executed to receive business change-event scope-related information and determine probable business software applications and business teams impacted by the business change-event based upon analysis of historical business change-event data. This system automates the discovery of impacts caused by business changes, such as a new business project, to improve the overall cycle-time for the change-event.

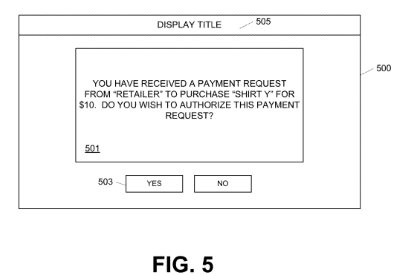

We’ll close up our survey of BofA’s recent innovations with a look at one more technology that leverages the ubiquity of mobile devices to help transfer money among people. U.S. Patent Application No. 20150066775, which is titled Transferring Funds Using Mobile Devices, discloses a method of determining a code usable to verify a transfer of funds from the financial account of a user, transmitting the code to a mobile device of the user, electronically receiving a request for transferring funds from the financial account to a point of sale system and initiating a transfer of funds to a seller account. A patent issued on this application would thrust the Bank of America firmly into the mobile banking field that Apple, Samsung and Google are already striving to dominate.

We’ll close up our survey of BofA’s recent innovations with a look at one more technology that leverages the ubiquity of mobile devices to help transfer money among people. U.S. Patent Application No. 20150066775, which is titled Transferring Funds Using Mobile Devices, discloses a method of determining a code usable to verify a transfer of funds from the financial account of a user, transmitting the code to a mobile device of the user, electronically receiving a request for transferring funds from the financial account to a point of sale system and initiating a transfer of funds to a seller account. A patent issued on this application would thrust the Bank of America firmly into the mobile banking field that Apple, Samsung and Google are already striving to dominate.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-early-bird-ends-Apr-21-last-chance-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

No comments yet.