Much of the world’s banking and financial systems rely upon the use of centralized clearing houses to verify transactions and make sure that money spent by a payer ends up in the coffers of a payee. When financial instruments such as securities or futures are traded between parties, the clearing house serves as a third-party intermediary to reduce the risk that one of the parties reneges on its financial commitment. Any readers who receive their salary or Social Security benefits through direct deposit do so through the automated clearing house (ACH) system operated by U.S. reserve banks or the Electronic Payment System.

Much of the world’s banking and financial systems rely upon the use of centralized clearing houses to verify transactions and make sure that money spent by a payer ends up in the coffers of a payee. When financial instruments such as securities or futures are traded between parties, the clearing house serves as a third-party intermediary to reduce the risk that one of the parties reneges on its financial commitment. Any readers who receive their salary or Social Security benefits through direct deposit do so through the automated clearing house (ACH) system operated by U.S. reserve banks or the Electronic Payment System.

Although these clearing houses are meant to reduce risk in financial transactions, they suffer from their own shortcomings. For example, securities which are difficult to liquidate could introduce risk into the system, making it difficult for a clearing house to satisfy a transaction in the case of a defaulting clearing member. A Harvard Business Law Review article published in April 2013 also explores the systemic risk created by the fragmentation of different clearing houses in jurisdictions around the world and issues related to imposing risk on creditors.

The concept of the central clearing house in financial systems could be completely obviated with the use of blockchain. Blockchain is a distributed database system that decentralizes the financial ledger; instead of the ledger being held and checked by the clearing house, each member of the blockchain network receives an updated ledger every time a transaction is made on the system. It’s a peer-to-peer system which reduces financial transaction risk through massive redundancy. With every member of the blockchain system holding a copy of the ledger for every transaction that has been completed, going back to the beginning of the blockchain, it becomes easier to identify malicious activity on the financial network or prevent transactions if users don’t have enough cryptocurrency. New transactions are recorded on blocks, which are added to the chain. The distributed nature of blockchain ledger gives them a high degree of immutability, meaning that it’s very difficult to change the ledger and that difficulty increases with each new block which is created. Blockchain systems like bitcoin often reward those who offer their computing resources to record new blocks; this incentivized process is known as mining.

![[[Advertisement]]](https://ipwatchdog.com/wp-content/uploads/2023/01/2021-Patent-Practice-on-Demand-1.png)

The reliability and validity of financial transactions in a blockchain is a function of a couple inherent features according to Raina Haque, founder of Erdos Intellectual Property Law and a lawyer specializing in parallel machines/computing and network technologies; she’s currently working with a client on drafting a patent application in the blockchain space. The decentralization and distribution of mining nodes in the network, the difficulty of the network’s mining method and the incentivizing of mining leading to a high number of mining nodes actively mining all support the reliability of a blockchain network. “Democratization of verification through accessible incentivization is central to the reliability of transactions on a blockchain,” Haque said. “Each transaction on a blockchain network is considered valid when it is included, by a miner, in a block. For an attacker to remove this transaction from the blockchain, they would have to remove the block in which it is contained.” In order to do that, the attacker would have to propose an alternate blockchain history, which starts before the block being attacked is created. But that alternate history will only be accepted if the alternate blockchain required more computational power to produce than the current chain, so as the ledger of a blockchain network grows and more transactions are recorded after the transaction targeted by an attacker, it becomes increasingly difficult to make a fraudulent transaction.

It’s expected that blockchain will become incorporated by a large number of financial institutions in the coming years. A survey of 90 asset owners and asset managers in the Asia Pacific region found that 65 percent expected to see blockchain technologies become widespread in the banking industry within five years. Some have opined upon whether blockchain’s data transparency could have prevented the bogus customer account scam recently perpetrated at Wells Fargo (NYSE:WFC). Last December, the U.S. Securities and Exchange Commission approved a stock trading framework proposed by Overstock.com, Inc. (NASDAQ:OSTK) to issue stock over the Internet via a blockchain system.

Now, major American banks are directing at least some research and development activities towards the world of blockchain. New York City-based financial institution Goldman Sachs (NYSE:GS) recently filed a patent application in the field of blockchain technologies. U.S. Patent Application No. 20160260169, entitled Systems and Methods for Updating a Distributed Ledger Based on Partial Validations of Transactions, would protect a method of modifying a data table which has a plurality of accounts in substantially real-time by receiving a request to modify an account, determining an identity of the validator which validates the request and modifying the data table if the request is validated. This innovation is intended to increase the degree of privacy which parties enjoy when making foreign exchange transactions.

Now, major American banks are directing at least some research and development activities towards the world of blockchain. New York City-based financial institution Goldman Sachs (NYSE:GS) recently filed a patent application in the field of blockchain technologies. U.S. Patent Application No. 20160260169, entitled Systems and Methods for Updating a Distributed Ledger Based on Partial Validations of Transactions, would protect a method of modifying a data table which has a plurality of accounts in substantially real-time by receiving a request to modify an account, determining an identity of the validator which validates the request and modifying the data table if the request is validated. This innovation is intended to increase the degree of privacy which parties enjoy when making foreign exchange transactions.

There is some controversy on the subject of developing blockchain systems which can be edited. Global professional services firm Accenture (NYSE:ACN) recently announced that it had filed patents in the U.S. and Europe for an editable blockchain system. Accenture notes that such ability to edit transactions is useful for permissioned systems involving major financial institutions in order to handle risk and regulatory concerns. The Accenture patent application hasn’t been published yet. For Goldman Sachs, the editable blockchain is desirable because of concerns surrounding the immediate publication of trades and how that can negatively affect a market maker. But in permissionless systems, such as Bitcoin, the inability of a central actor to change the ledger is one of the ways that the decentralized system ensures security in transactions. This conflict is good indicator of how regulatory concerns will impact digital cryptocurrency technologies in the years to come.

For knowledgeable insiders like Haque, the central authority in permissioned blockchain systems constitutes an undermining of the traditional concept. “I am concerned that some entities are either talking up their use of blockchain to ride the hype and gain the favor of the public or are being sold blockchain technology like snake oil,” Haque said. Highly centralized blockchains cannot have the reliability, immutability and transparency of decentralized blockchains and might not win favor from a blockchain-savvy crowd, she notes. “I have yet to see a publication or any news coverage that sells me on blockchains with a centralized editing authority, but I keep an open mind because you never know what genius idea is in the pipeline.”

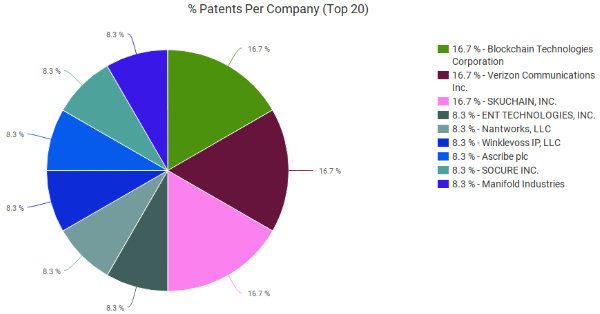

Currently, the industry is an open sector of technological innovation according to the patent analysis tools available at Innography. The U.S. Patent and Trademark Office has only granted 16 patents and published another four patent applications related to blockchain as of September 23rd. There are three companies with an even 16.7 percent share of the blockchain patent market in the U.S.: Blockchain Technologies Corporation of New York City; Verizon Communications (NYSE:VZ), also of NYC; and Skuchain Inc. of Mountain View, CA. However, each of these entities only hold two U.S. intellectual property assets in this field. “This is a great space for patent attorneys with a computer/software engineering tech background,” Haque said. “It’s new and moving at a breakneck speed. There is significant diversity in the top minds of this space too, including diversity in gender, age, nationality and race. Time will tell, but I have every reason to believe that diving into this space is taking an opportunity to make a historical mark.”

Currently, the industry is an open sector of technological innovation according to the patent analysis tools available at Innography. The U.S. Patent and Trademark Office has only granted 16 patents and published another four patent applications related to blockchain as of September 23rd. There are three companies with an even 16.7 percent share of the blockchain patent market in the U.S.: Blockchain Technologies Corporation of New York City; Verizon Communications (NYSE:VZ), also of NYC; and Skuchain Inc. of Mountain View, CA. However, each of these entities only hold two U.S. intellectual property assets in this field. “This is a great space for patent attorneys with a computer/software engineering tech background,” Haque said. “It’s new and moving at a breakneck speed. There is significant diversity in the top minds of this space too, including diversity in gender, age, nationality and race. Time will tell, but I have every reason to believe that diving into this space is taking an opportunity to make a historical mark.”

Many readers might be most familiar with bitcoin, the blockchain technology that has arguably made the greatest inroads towards becoming a mainstream cryptocurrency. However, bitcoin is only one cryptocurrency system that makes use of blockchain as its underlying technology. There are several alternatives to bitcoin, which use blockchain technology, some which claim to offer higher security or claim to have fairer block mining practices.

The use of distributed ledger technologies is not limited to the financial sector. Reports of a note to clients distributed by Goldman Sachs indicate a wide array of uses for blockchain, including verifying online identities on peer-to-peer platforms like Airbnb, enabling distributed energy systems where homeowners can sell electricity to other homeowners and even reducing administrative costs in real-estate transactions. Although purists may not be entirely thrilled with permissioned systems being developed, the sector will grow in the years to come. A market report issued this May by BI Intelligence predicts that spending on capital markets applications of blockchain will increase by a compound annual growth rate of 52 percent through 2019, when the sector will be worth $400 million. Haque also noted Artlery, a platform designed to increase engagement with the fine art market for both customers and creatives, and Synereo, which uses blockchain as the underlying technology for a social network. Haque recommended Blockchain Revolution by Don and Alex Tapscott as a great non-technical primer, although development in the field was moving so fast that this book, released in May, is already a little dated.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-early-bird-ends-Apr-21-last-chance-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

No comments yet.