“Strategic advantages in securing investment can clearly be realized from early and tandem pursuit of an Orphan Drug Designation and patent protection.”

Rare Disease Awareness Ribbon.

Drug innovators are providing much needed focus on rare diseases and, at the same time, leveraging early-stage rare disease results to facilitate down-stream market entry in broad-spectrum diseases. This paper provides a data-based demonstration of how early- and mid-stage pharmaceutical companies are using the Orphan Drug Program—in combination with pursuing patent portfolio protection—to secure investment and de-risk their platforms, thus lowering the financial barrier for expanding their product pipeline.

The Orphan Drug Program—which is available for drugs that treat diseases affecting fewer than 200,000 patients annually in the United States—provides a number of incentives that can lower the barrier for successfully getting a drug to market. For instance, due in part to the reduced size of clinical trials associated with rare diseases, gaining regulatory approval for treating rare diseases is widely perceived to be simpler and more cost-effective than gaining approval for broad-spectrum diseases. Indeed, the Food and Drug Administration (FDA) allows a number of alternative clinical trial designs to meet approval standards, and orphan drugs are also more likely to qualify for expedited review and approval procedures. On top of this, orphan drugs are eligible for a 25% tax credit for clinical trial expenses (which can be claimed up to 20 years after receipt of the designation, and can in some instances be applied to offset payroll taxes), eligibility for research grants, waiver of FDA user fees, and a seven-year post-approval market exclusivity.

Before receiving FDA approval to market a rare disease treatment, innovators must obtain an Orphan Drug Designation (ODD) signaling their intent to pursue approval of an orphan drug. Seeking an ODD is a relatively quick and low-cost process; the FDA endeavors to respond to newly-submitted ODD requests within 90 days of receipt, and there is no FDA fee for requesting the designation. Moreover, the application can be submitted anytime during the drug development process, as long as the applicant can provide “a scientific rationale to establish a medically plausible basis for the use of the drug for the rare disease . . . .” (21 C.F.R. § 316.20(b)(4)).

While the Orphan Drug Program provides valuable benefits at early stages of drug development to qualifying applicants, longer term gains require FDA approval (i.e., more than just receiving a designation) and are limited by narrowly-defined patient populations. More robust exclusivity can be achieved through the U.S. patent system, namely, the right to exclude others from making, using, offering for sale, or selling the invention throughout the United States or importing the invention into the United States, for a period of 20 years. Initiating and securing an IP portfolio is generally more expensive and time-intensive than obtaining an ODD (e.g., the U.S. Patent and Trademark Office (USPTO) endeavors to grant a patent within three years following submission of a patent application); however, the protections can be broader and more versatile, including coverage for use of an orphan drug active agent in other, non-rare, diseases. Leveraging an ODD for increased investment at early stages can provide additional funds needed for further product development and IP protection, which can be leveraged in turn for higher-dollar funding rounds.

The Financial Benefits of Orphan Drug Designations and Granted Patents

To assess the impact of obtaining an ODD and/or granted patent on private investment, we evaluated publicly available funding data associated with private rare disease companies. In particular, using calendar year 2017 as a snapshot (in 2017 the FDA issued 479 ODDs to over 350 applicants), we utilized Crunchbase® data to tabulate funding information for private companies that received an ODD. We cumulated funding data (such as grants, angel rounds, seed rounds, venture rounds, debt financing, etc.) across the lifetime of the identified companies, and then cross-referenced this data with both granted patents (listing the company as an assignee or applicant) and ODDs (including ODDS received by the companies in 2017 and also in calendar years other than 2017) to determine the financial impact of achieving an ODD or patent.

Noting that: (i) many 2017 ODD applicants were publicly traded and (ii) not all privately-held companies release funding information, we identified 92 companies with publicly available funding data in Crunchbase®. Across the 92 companies, Crunchbase® included data for over 200 distinct funding rounds.

As a conservative cutoff, we considered that any funding event announced within one year of the ODD or patent grant date to be “associated with” the designation or grant. We excluded funding rounds in which the amount raised was not publicly disclosed, and we excluded acquisitions from the data analysis. We acknowledge some limitations in our data set. For one, the data does not account for exclusively licensed patents where the company is not listed as an assignee or applicant. For instance, we identified a $70 million funding round associated with a patent licensed from a university to a company; this funding round was nevertheless counted as not associated with an ODD or patent in our data analysis. We also identified a $49.5 million funding round with a press release particularly stressing the importance of an ODD; however, this funding round was announced more than one year after the ODD date, and so it was counted as not associated with an ODD or patent in our data analysis.

Turning to the data, we found that more than half of the companies we evaluated reported funding associated with receipt of an ODD or patent grant. Moreover, such events have a striking impact on the average amount of funding the companies received. In this regard, on average, funding rounds associated with an ODD or patent grant were reported to raise almost three times the dollar amount as compared to funding rounds not associated with such events (see Figure 1). The median funding rounds trended similarly.

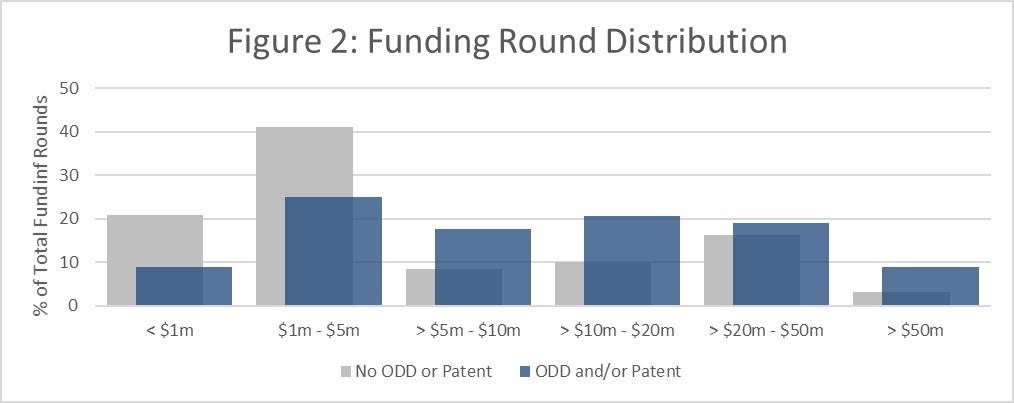

As can be seen by binning the above-mentioned funding rounds by dollar amount, the increased average funding round can be attributed to an upward shift in the relative percentage of high-dollar investments following receipt of an ODD or granted patent (see Figure 2). That is, almost half the funding rounds associated with an ODD or patent grant raised more than $10 million. On the other hand, over 60% of funding rounds not associated with a designation or grant raised $5 million or less.

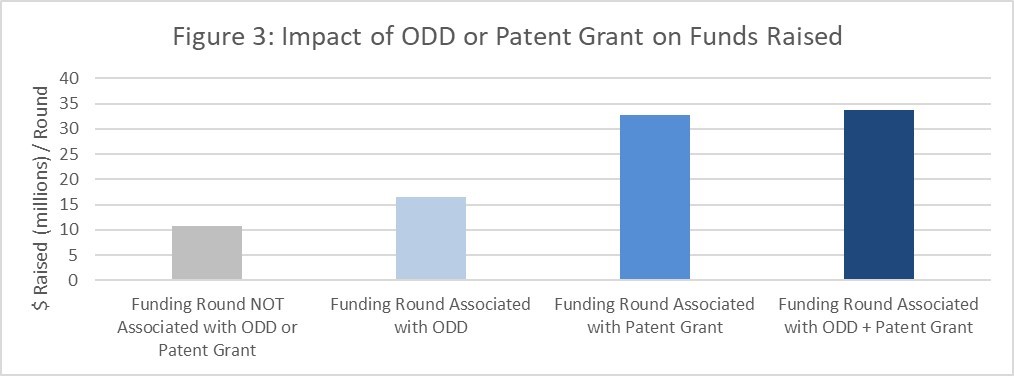

To parse out the individual impact of ODDs and patent grants, we calculated the average funding rounds associated with: (i) only receiving an ODD (i.e., without an associated patent grant), (ii) only receiving a patent grant (i.e., without an associated ODD), and (iii) receiving both an ODD and a patent grant. As shown in the Figure 3, an ODD was associated with an approximately $6 million bump in average funding rounds as compared to funding rounds without a designation or a patent grant. Obtaining a granted patent—either with or without a concomitant ODD—was associated with an approximately $20 million increase as compared to the same reference.

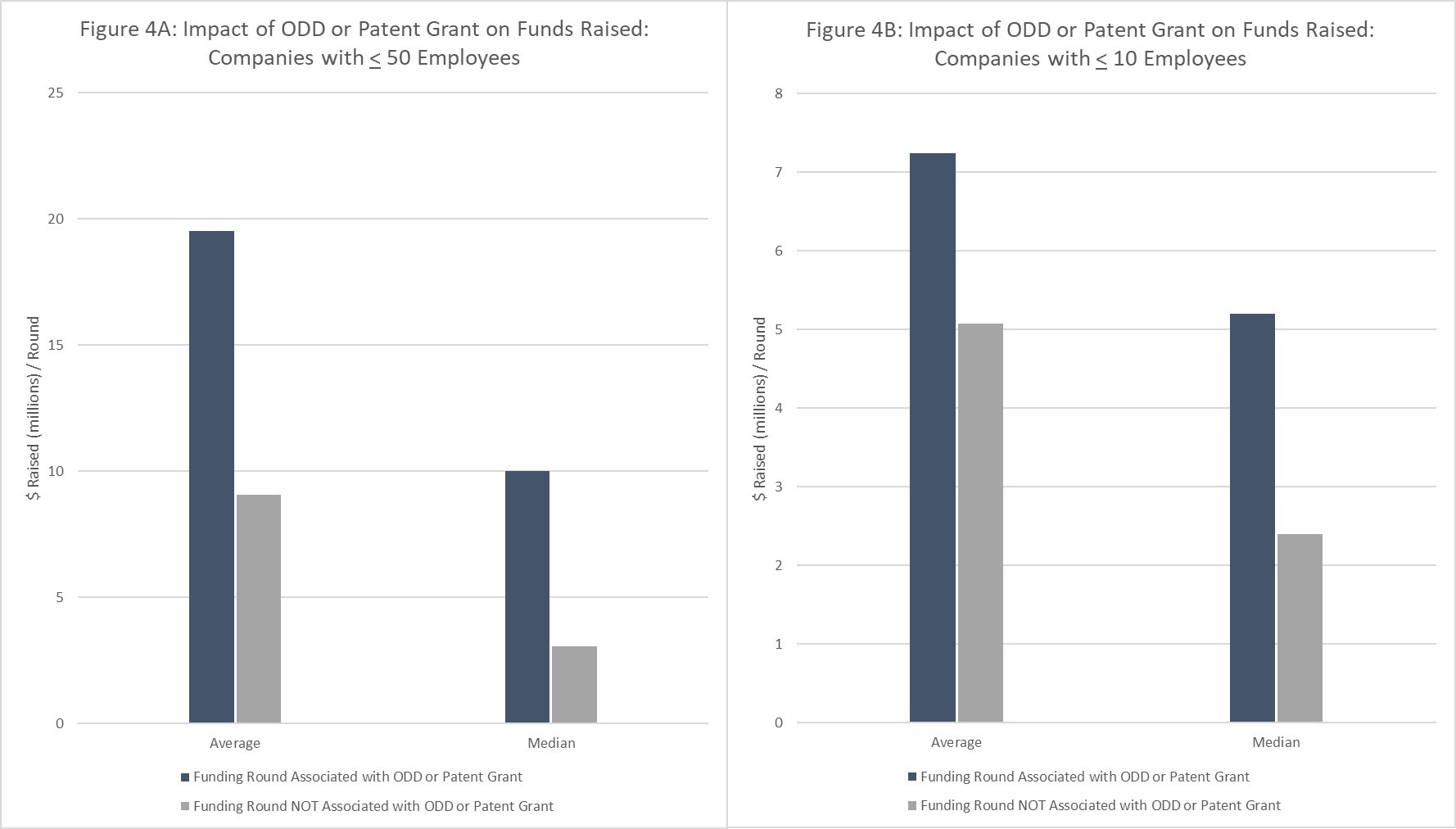

Lastly, we evaluated the impact of receiving an ODD or patent grant on private companies with 50 employees or less, and separately, private companies with 10 employees or less (company size was determined using either Crunchbase® or D&B HooversTM; companies in which a size was not listed were excluded). As shown in the Figures 4A-B, in both cases receiving an ODD or granted patent was associated with a marked increase in average and median funding round amounts.

More specifically, in companies with 50 employees or less, obtaining an ODD or patent grant was associated with an approximately $10 million increase in average funding round, and in companies with 10 employees or less it was associated with an increase of over $2 million per funding around.

Multi-level Protection: Combining an ODD with USPTO-Based Exclusivity

As shown here, strategic advantages in securing investment can clearly be realized from early and tandem pursuit of an ODD and patent protection. Moreover, orphan drugs can provide an effective market entry strategy and pave the way for downstream commercialization of the same product for broader spectrum disease. Perhaps as a result of the strategic value of pursuing rare disease indications, the number of ODDs has surged in recent years, with subsequent orphan drugs approvals accounting for about 58% of new drugs approved in 2018. This is a win for both patients and innovators working to bring new drugs to market.

Image Source: Deposit Photos

Vector ID: 283342040

Copyright: Tacka

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/03/IP-Copilot-Apr-16-2024-sidebar-700x500-scaled-1.jpeg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-early-bird-ends-Apr-21-last-chance-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

No comments yet.